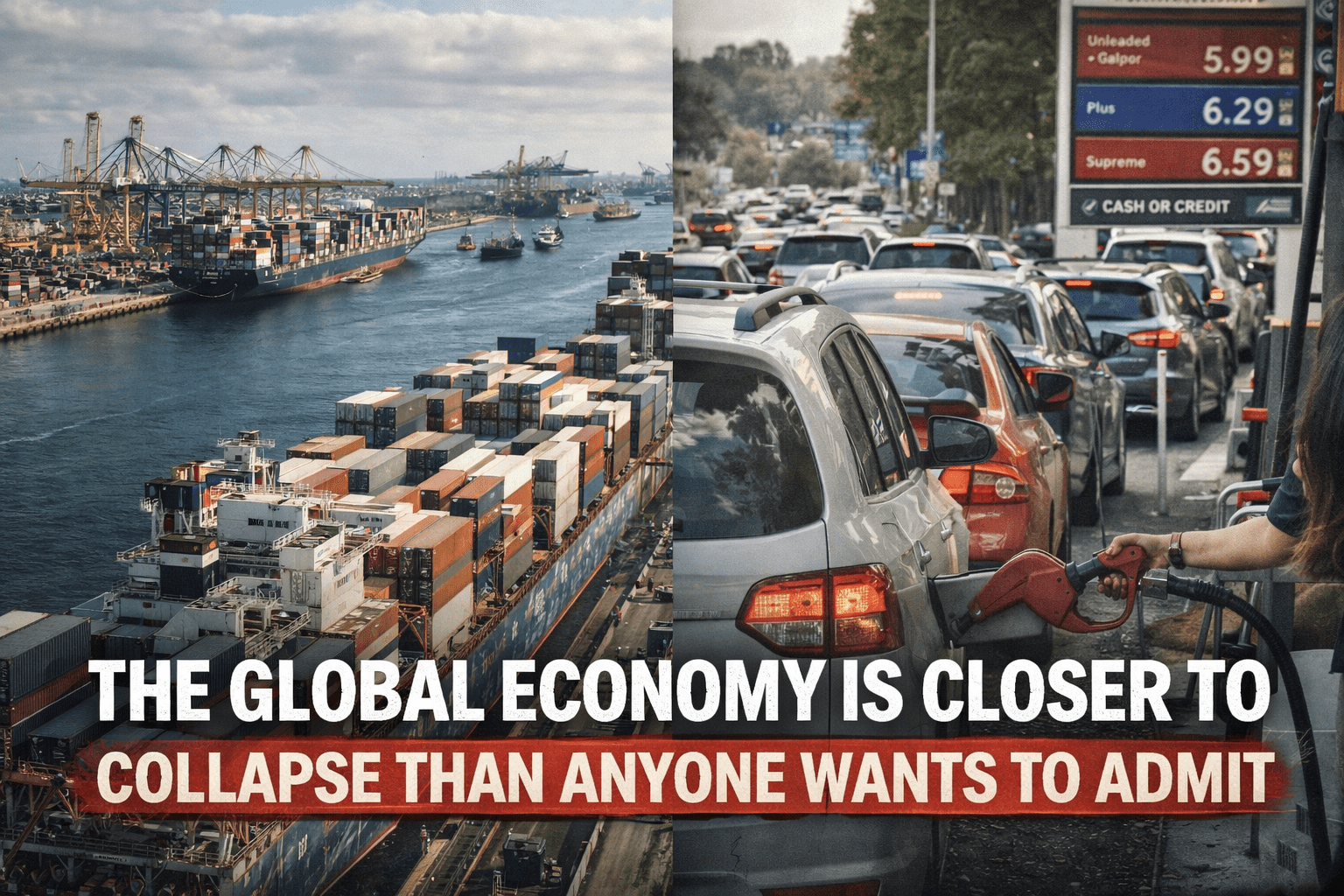

When disruptions strike the deepest layers of the global economy, their consequences do not arrive with spectacle but with delay. The most destabilizing feature of a systemic shock is often not its immediate violence but the deceptive calm that follows it. Cargo vessels already underway continue to reach their destinations, warehouses continue to dispatch inventory manufactured months earlier, and supermarket shelves remain stocked with goods produced in a previous season under conditions that no longer exist. This temporal inertia creates an illusion of stability at precisely the moment when the foundations of that stability are eroding. In the case of escalating conflict affecting energy infrastructure across the Gulf and maritime passage through the Strait of Hormuz, the world is experiencing this quiet interval between cause and consequence, a period in which daily life appears normal while the logistical arteries of the global system are progressively constricted.

The Strait of Hormuz is not merely a geographic feature but a structural dependency embedded into modern economic life. A significant share of globally traded oil, liquefied natural gas, petrochemical feedstocks, and refined fuels must transit this narrow corridor. The global economy is therefore organized around the assumption that passage through this route will remain uninterrupted, predictable, and secure. Insurance contracts, shipping schedules, refinery throughput, agricultural input planning, and manufacturing procurement cycles all incorporate this assumption. When that assumption is violated, the disturbance propagates outward in complex ways that are not immediately visible to consumers or even to many policymakers. What appears to be a regional disruption is, in practice, a stress event for a system designed around continuous flow.

The first reason the impact is not felt immediately lies in the layered structure of supply chains. Energy commodities are extracted, processed, shipped, stored, refined, transformed into industrial inputs, embedded into manufactured goods, transported again, warehoused, distributed, and finally sold. At each stage, inventories exist that can temporarily mask interruptions upstream. Tankers that departed weeks before escalation continue to arrive. Refineries operate on crude reserves already purchased. Manufacturers draw on stored plastics, chemicals, and packaging materials. Retailers sell goods assembled under prior conditions. This buffering capacity is often interpreted as resilience, yet it is better understood as delay. It postpones the visible manifestation of stress without removing its cause.

The second reason for delayed impact lies in the degree to which modern economies depend on energy not only as fuel but as material. Oil and gas are not simply burned; they are transformed into plastics, synthetic fibers, fertilizers, solvents, coatings, adhesives, and industrial intermediates that form the physical substance of modern life. When energy infrastructure is damaged or shipping lanes are restricted, the effect is not limited to electricity generation or transportation costs. It extends into the availability of packaging, textiles, construction materials, medical supplies, and agricultural inputs. Because these materials are embedded into complex production processes, shortages do not appear as immediate absences but as gradual constraints that slow manufacturing, raise costs, and reduce output over time.

A third factor contributing to the illusion of continuity is the seasonal nature of agriculture. The food being consumed today was largely planted, fertilized, harvested, processed, and transported under last year’s conditions. Farmers made input decisions months earlier based on expectations of fertilizer availability, diesel prices, and shipping reliability that no longer hold. The current stability of food supply therefore reflects past logistical conditions, not present ones. If fertilizer shipments are delayed now, the consequences will be visible at harvest, not at planting. If diesel prices remain elevated, the effects will appear in distribution costs months later. The food system, like manufacturing, operates on a time lag that separates disruption from consequence.

Caught on Camera: What the Government DOESN’T Want You to See Inside This Home!

The fragility of this arrangement becomes clearer when examining the role of natural gas in fertilizer production through the Haber–Bosch process. Natural gas is converted into ammonia, ammonia into urea, and urea into the nitrogen fertilizer essential for high-yield agriculture. This chain links energy infrastructure in the Gulf directly to crop yields in distant agricultural regions. Interruptions to gas processing facilities, export terminals, or shipping routes therefore reverberate into farming decisions across continents. Yet because planting cycles and biological growth take time, these reverberations are delayed, emerging only when it is too late to reverse seasonal losses.

Fuel markets provide the earliest and most visible economic signal of disruption. Diesel, in particular, functions as the mechanical bloodstream of industrial economies. It powers heavy transport, agricultural machinery, construction equipment, and freight logistics. When diesel prices rise, the effect is transmitted to nearly every category of goods through higher shipping costs. Logistics firms introduce fuel surcharges, delivery services adjust pricing, and manufacturers pass costs downstream. Consumers rarely associate the price of household items with fluctuations in diesel markets, yet the relationship is direct and structural. Over time, elevated fuel costs become embedded in retail prices, contributing to broader inflationary pressure that is difficult to isolate or reverse.

This cost transmission is gradual rather than abrupt. A shipping company does not immediately double its rates; it adds a surcharge. A retailer does not replace an entire price list overnight; it adjusts gradually as inventory turns over. A manufacturer absorbs some costs temporarily before raising prices. The cumulative effect, however, is persistent upward pressure across multiple sectors simultaneously. Because these adjustments occur incrementally, they can be misinterpreted as routine market fluctuation rather than symptoms of systemic stress originating far upstream in disrupted energy corridors.

Another critical but less visible dimension of the crisis lies in petrochemical supply chains. Plastics and synthetic materials depend on feedstocks derived from oil and gas, many of which originate in the Gulf. Compounds such as monoethylene glycol and purified terephthalic acid are foundational for producing PET plastics and polyester fibers used in packaging, clothing, medical supplies, and industrial materials. Disruptions to refining, processing, or shipping therefore threaten the availability of materials embedded in countless products. Unlike fuel shortages, which are immediately noticeable, petrochemical shortages manifest as delays in manufacturing, reduced product availability, or increased prices months later when inventories are exhausted.

The interconnected nature of these systems means that stress multiplies as it propagates. Transportation depends on fuel. Packaging depends on plastics. Manufacturing depends on packaging and transportation. Agriculture depends on fertilizer and fuel. Retail depends on all of the above. When multiple nodes in this network are strained simultaneously, the effects compound rather than add. The result is not a single shock but a sustained period of cost escalation and supply constraint that becomes increasingly difficult to mitigate as time passes.

Perhaps the most challenging aspect of such a crisis is psychological and political rather than logistical. The absence of immediate scarcity encourages complacency. Policymakers and consumers alike may underestimate the severity of disruptions because daily life appears largely unchanged. This perception delays corrective action and complicates communication about risk. By the time shortages and price spikes become undeniable, the processes set in motion months earlier have already limited available options. Agricultural cycles cannot be reversed, damaged infrastructure cannot be rebuilt instantly, and alternative supply routes cannot be created overnight.

Even if maritime passage through the Strait of Hormuz were restored quickly, the damage to infrastructure, insurance markets, shipping schedules, and industrial planning would persist. Refineries and processing plants require time to repair. Shipping firms require time to reestablish routes and contracts. Manufacturers require time to rebuild inventories of raw materials. The economic system does not return to prior equilibrium immediately; it enters a prolonged period of adjustment characterized by higher costs and reduced efficiency.

What makes this situation particularly significant is that it exposes the structural trade-offs of globalization. Efficiency has been achieved by concentrating production of essential inputs in regions where they can be produced most cheaply and shipped reliably. This concentration reduces redundancy and lowers costs under stable conditions but increases vulnerability when key nodes are disrupted. The very architecture that enabled affordable goods and rapid global trade becomes a source of fragility when continuity of flow is interrupted.

The present moment, therefore, is defined not by visible collapse but by hidden contraction. The goods on shelves, the fuel in stations, and the food in markets reflect a world that existed months ago. The world that exists now is one in which energy corridors are uncertain, infrastructure is damaged, shipping routes are contested, and industrial planning assumptions have been invalidated. The consequences of this shift will not appear all at once but will emerge gradually across sectors in the form of rising costs, constrained availability, and persistent economic pressure.

Understanding this delay is essential to understanding the scale of the risk. The most dangerous phase of a systemic disruption is often the quiet interval before its effects are widely felt, when the illusion of continuity obscures the erosion of underlying capacity. In this interval, the global economy continues to move forward on momentum alone, unaware that the logistical and material foundations supporting that movement are steadily weakening.

Industrial refinery at dusk with flaring stacks and dense pipework

The transformation of an energy disruption into a generalized cost-of-living crisis does not occur through a single dramatic rupture but through a sequence of quiet adjustments that ripple across sectors. What begins as uncertainty in maritime transit through the Strait of Hormuz evolves into higher insurance premiums for shippers, longer routing times for tankers, reduced refinery throughput, and increased wholesale fuel prices. These changes, initially visible only to traders, logistics coordinators, and procurement managers, gradually pass into the pricing structures of transport firms, manufacturers, wholesalers, retailers, and ultimately households. The path from geopolitical disruption to supermarket receipt is neither linear nor immediate, yet it is structurally inevitable in an economy whose material circulation depends on affordable and predictable energy.

Diesel occupies a uniquely consequential position in this transmission chain. Unlike gasoline, which is closely associated with private mobility, diesel underpins freight, agriculture, construction, maritime support, and industrial logistics. When diesel prices rise, the effect is not confined to one consumer behavior but distributed across nearly all physical commerce. Every pallet moved from a port, every harvested field, every construction site, and every delivery vehicle reflects diesel’s price. As transport operators confront rising fuel expenses, they implement surcharges rather than outright rate revisions, a strategy that obscures the systemic nature of the increase. These surcharges accumulate across stages of distribution, each small enough to appear manageable, yet collectively sufficient to elevate the price of nearly all goods.

This phenomenon illustrates how inflation driven by energy constraints differs from demand-driven inflation. It is not the result of excessive purchasing power but of constrained material throughput. Manufacturers do not raise prices because consumers are buying more; they raise prices because moving inputs and outputs costs more. Retailers do not adjust prices because of increased margins but because replacement inventory arrives with higher embedded costs. The visible symptom—higher prices—resembles conventional inflation, but the underlying cause is physical constraint within energy and logistics networks.

Petrochemicals represent a second, less visible conduit for cost transmission. Plastics, synthetic fibers, and industrial polymers rely on feedstocks derived from oil and gas processing, much of which is concentrated in Gulf production zones. Compounds such as monoethylene glycol and purified terephthalic acid are essential for manufacturing PET plastics and polyester textiles that permeate packaging, clothing, medical supplies, and consumer goods. When production or shipment of these inputs is disrupted, manufacturers initially draw on stored inventories. As these reserves deplete, procurement becomes more expensive and uncertain. Production schedules slow, substitute materials are sought at higher cost, and finished goods carry increased prices that seem unrelated to energy markets but are, in fact, directly linked.

The packaging industry provides a clear example of this linkage. Food distribution depends heavily on plastic containers, films, and seals to preserve freshness and enable long-distance transport. If plastic resins become scarce or more expensive, the cost of packaging rises, and with it the cost of food distribution. This increase is not immediately visible as a “plastic shortage” but manifests as incremental price adjustments in groceries. Consumers rarely associate higher food prices with petrochemical feedstock disruptions, yet the relationship is embedded within the supply chain.

Agriculture introduces an even more consequential dimension through its dependence on nitrogen fertilizers synthesized via the Haber–Bosch process. Natural gas is transformed into ammonia, then into urea, which is applied to crops to sustain high yields. When natural gas processing and export capacity in the Gulf region is impaired, fertilizer shipments are delayed or reduced. Farmers, facing uncertainty, may reduce application rates or planted acreage. These decisions, made months before harvest, determine the volume of food entering global markets later in the year. By the time consumers observe higher prices for grains, meat, and processed foods, the causal chain linking those prices to earlier energy disruptions is no longer obvious.

This delayed manifestation complicates economic interpretation. Observers may attribute rising food costs to weather patterns, market speculation, or currency fluctuations, overlooking the upstream energy constraints that influenced fertilizer availability and diesel costs during planting and harvesting. Yet the sequence is structurally coherent: constrained energy affects fertilizer production and farm operations, which affects yields, which affects food supply, which affects prices. Each step introduces a temporal gap that obscures the origin of the problem.

Logistics firms further propagate these pressures through fuel surcharges applied to shipping services. Postal carriers, courier networks, and freight companies adjust pricing formulas to account for elevated fuel expenditures. E-commerce platforms and retailers then pass these increases to sellers and consumers. Because such surcharges are framed as temporary or situational, they do not immediately signal systemic stress. However, if elevated energy costs persist, these adjustments become normalized, embedding higher transport costs permanently into the price structure of goods.

An important feature of this process is its asymmetry. Prices adjust upward quickly in response to higher costs but rarely return fully to previous levels even if conditions improve. Businesses, having adapted to new cost baselines, are reluctant to reduce prices in uncertain environments. Thus, a temporary energy disruption can leave a lasting imprint on price structures across sectors. The economic system ratchets upward, and households experience a sustained reduction in purchasing power.

This dynamic unfolds against a backdrop of preexisting cost-of-living strain. In many regions, food, housing, and transportation expenses had already outpaced wage growth before energy disruptions intensified. Additional cost pressures from fuel, packaging, logistics, and agriculture therefore compound an already fragile economic balance. Consumers respond by reducing discretionary spending, which in turn affects sectors unrelated to energy, creating secondary economic effects that ripple through employment and investment patterns.

The psychological dimension of this process is as significant as the material one. Because price increases appear gradually across diverse categories, they are often perceived as unrelated events rather than components of a single systemic disturbance. This perception inhibits coordinated policy responses and delays recognition of the structural nature of the problem. By the time the connection between energy disruption and widespread inflation becomes clear, many of the contributing processes—missed fertilizer applications, depleted petrochemical inventories, restructured shipping routes—have already run their course.

Even if maritime transit through the Strait of Hormuz stabilizes, the economic adjustments made during the disruption persist. Insurance costs remain elevated, shipping contracts reflect revised risk assessments, and manufacturers maintain higher inventory buffers at greater expense. The system does not revert to its previous equilibrium but settles into a new configuration characterized by higher baseline costs and reduced efficiency.

In this way, an energy shock becomes everyday inflation not through sudden scarcity but through the quiet, cumulative transmission of cost across interconnected systems. The supermarket receipt, the delivery fee, and the price tag on household goods become the final expressions of a chain of events that began far upstream in disrupted energy corridors and contested maritime routes. Understanding this chain is essential for recognizing that what appears to be routine price fluctuation is, in fact, the economic surface of a deeper structural disturbance.

Vast agricultural field at sunrise with mechanized fertilizer application

The most consequential effects of energy and shipping disruptions do not emerge first in cities, ports, or markets, but in fields whose condition will only be measured months later at harvest. Agriculture operates according to biological schedules that cannot be paused, accelerated, or rescheduled in response to geopolitical instability. Seeds must enter the soil within narrow climatic windows, fertilizers must be applied at precise stages of growth, irrigation and mechanized labor must proceed on time, and harvested crops must move quickly into storage and distribution. When any of these steps are compromised by constrained access to fuel or fertilizer, the resulting losses are not immediately visible. They are embedded into the growing season itself, maturing silently until harvest reveals the cumulative effect.

This temporal rigidity makes farming uniquely vulnerable to disruptions linked to the Strait of Hormuz. A substantial share of globally traded ammonia and urea—critical nitrogen fertilizers—originates from producers in the Gulf region. These products are synthesized using natural gas through the Haber–Bosch process, a century-old industrial method that remains indispensable to modern food production. When gas processing plants, export terminals, or shipping routes are impaired, fertilizer deliveries fail to arrive on schedule in agricultural regions far removed from the conflict zone. Farmers, confronted with uncertainty, must either reduce application rates or delay planting, both of which lead to lower yields.

Unlike manufacturing delays, agricultural losses cannot be recovered later in the year. A missed fertilizer window cannot be corrected once crop growth advances beyond the stage where nitrogen uptake is effective. A planting delay cannot be reversed once seasonal temperature patterns shift. The harvest reflects decisions and constraints imposed months earlier, at a time when supermarket shelves still appeared fully stocked and economic life seemed unaffected. By the time reduced yields manifest as higher food prices, the causal chain linking those prices to earlier energy disruptions has faded from public awareness.

The implications extend beyond staple grains. Livestock production depends on feed crops such as corn and soy, which in turn depend on fertilizer and diesel-powered farming equipment. Reduced yields in feed crops raise costs for meat, dairy, and processed foods, transmitting agricultural strain into multiple dietary categories. Food processing facilities, already facing higher packaging and transport costs due to petrochemical and diesel price pressures, must now contend with more expensive raw inputs. Retail prices rise accordingly, and food affordability declines across income levels.

Perennial crops such as olives, grapes, and certain fruits are less sensitive to annual fertilizer cycles, yet they too depend on transportation, packaging, and energy-intensive processing. No segment of the food system is fully insulated from the broader material constraints imposed by energy disruption. The difference lies only in timing: annual crops feel the impact first through yield reductions, while perennial crops experience it through higher processing and distribution costs.

This agricultural dimension underscores a broader truth about modern economies: they are materially dependent in ways that are easy to overlook during periods of stability. Food, packaging, textiles, construction materials, and consumer goods all trace their origins back to energy extraction, petrochemical transformation, and industrial synthesis concentrated in specific geographic regions. The disruption of these regions does not immediately halt economic activity but gradually constricts the flow of materials necessary to sustain it. The result is a slow tightening rather than a sudden break.

As inventories of plastics, chemicals, and fertilizers diminish, industries begin competing for limited supplies. Prices rise not only because of higher production costs but because scarcity introduces bidding dynamics into procurement markets. Smaller firms and lower-income regions are often the first to feel the strain, unable to secure inputs at rising prices. This uneven distribution of impact contributes to widening economic disparities both within and between countries.

The persistence of these effects even after partial restoration of shipping routes or infrastructure reveals another critical feature of systemic disruption: recovery is slower than decline. Refineries, processing plants, and fertilizer facilities require extensive time to repair and restart. Shipping networks must renegotiate contracts, insurance terms, and routing patterns. Manufacturers rebuild inventories cautiously, wary of renewed disruption. Farmers, having endured one season of uncertainty, adjust future planting decisions conservatively. The system does not rebound to its previous state but enters a prolonged phase of reduced efficiency and higher baseline costs.

Psychologically, the lag between disruption and consequence creates a false sense of security. The absence of immediate shortages encourages the belief that systems are more resilient than they truly are. This perception delays adaptation and reduces urgency in addressing structural vulnerabilities. By the time food prices, product availability, and economic stress become widely apparent, the processes responsible for them have been unfolding for months beyond easy correction.

The events surrounding the Strait of Hormuz therefore illuminate a central paradox of globalization. The efficiency achieved through concentrated production and tightly synchronized logistics reduces costs under stable conditions but amplifies fragility when key nodes are disrupted. The global economy’s ability to function smoothly depends on uninterrupted flow through a small number of critical corridors. When those corridors are compromised, the consequences are distributed widely but felt gradually, obscured by the inertia of inventories and seasonal cycles.

Ultimately, the most significant outcome of such disruption is not a dramatic collapse but a sustained period of constraint. Higher food prices, elevated transport costs, reduced material availability, and persistent inflationary pressure become the new normal. Households adjust by reducing discretionary spending, businesses adapt by passing costs forward, and governments confront the challenge of managing economic stress whose origins lie far beyond domestic policy.

In this sense, the long shadow of energy and shipping disruption falls not as a sudden darkness but as a lengthening twilight. The world continues to move, goods continue to circulate, and markets continue to operate, yet each does so under progressively tighter material limits. What appears at first as a temporary disturbance reveals itself over time as a structural shift, reshaping the economic landscape through gradual, cumulative pressure rather than immediate rupture.

The latest street interview questions at the No Kings rallies are now focused on discrimination against the gays of Hormuz because they say that the Straights of Hormuz have been getting all of the attention. https://www.youtube.com/shorts/eLGejY_D9RY

LikeLike

They are paving the way for the NWO!

All fiat collapses over time and the globalist bankers know this and are pushing their governments to expedite “digital ID” upload to access the internet where the coming digital money will be stored and utilized!:

🇲🇽 CELLPHONE DATA 🔸MEXICO (2026)

The “straight” will remain closed until food rationing becomes global and a global cyber-attack is done to force “digital ID” to access the internet:

Food Rationing Warnings in Australia + “World-Shaking” Cyberattack Alert: Time to Grow

They are following the covid script folks!:

PROBLEM: War → REACTION: Lockdown → SOLUTION: New World Order…The Plan UNVEILED!!!!

The globalists fully intend to initiate their next sacrifice as this exsatanist proves their rituals in 5 minutes!:

SATANIC SEASON OF SACRIFICE RITUAL ☠️

The war in the middle east is fulfilling Albert Pike’s vision of the 3rd world war in his letter where mutual destruction is the desired outcome to destroy religion:

Albert-Pike-Letter-to-Mazzini-3.pdf

“The Third World War must be fomented by taking advantage of the differences caused by the “agentur” of the “Illuminati” between the political Zionists and the leaders of Islamic World. The war must be conducted in such a way that Islam (the Moslem Arabic World) and political Zionism (the State of Israel) mutually destroy each other.

The timeline in this video is being fulfilled:

IPETGOATII

Globalists such as Austen Carlsten of the BIS proves in 1 minute their plans for total control of buying and selling will be in their hands once this digital prison is fully uploaded:

Agustin Carstens, (Bank of International Settlements), explains “the benefits” of the CBDC

Please listen to one of Austen Carlsten’s bankster buddies over at the IMF tell us in the 38 second video embedded in this link, that to enter the NWO ~ “New World Order” everyone will be required to have a smart phone, bank account, and upload their digital ID:

https://sociable.co/government-and-policy/digital-id-bank-account-smartphone-new-world-imf-spring-meetings/

The Vietnamese banks with their government stooges just stole 86 million bank accounts of those who didn’t upload their digital ID by 9/1/2025 as this Vietnamese economist proves in 1 minute:

https://www.youtube.com/shorts/sSESYsiw0tU

We were already warned by David Webb who showed how tokenization is going to digitize everything, so your digital ID is the only way to claim ownership as this 12 minute video proves:

The Great Taking and the Tokenization of Everything

Please do NOT upload your digital ID as that is giving the beast system your mark to buy and sell:

The Mark of the Beast | Sum Of Thy Word

We are already in the 2nd half of the timeline within this link folks so prepare accordingly!:

The Rapture of the Church is After the Tribulation | Sum Of Thy Word

LikeLike